| 1. Multinational Corporations | |

| Definition of MNC |

Multinational firms arise because capital is much more mobile than labor. Since cheap labor and raw material inputs are located in other countries, multinational firms establish subsidiaries there. They are often criticized as being runaway corporations. Economists are not in agreement as to how multinational or transnational corporations should be defined. Multinational corporations have many dimensions and can be viewed from several perspectives (ownership, management, strategy and structural, etc.) The following is an excerpt from Franklin Root, International Trade and Investment |

| Ownership criterion | Some argue that ownership is a key criterion. A firm becomes multinational only when the headquarter or parent company is effectively owned by nationals of two or more countries. For example, Shell and Unilever, controlled by British and Dutch interests, are good examples. However, by ownership test, very few multinationals are multinational. The ownership of most MNCs are uninational. (e.g., the Smith-Corona versus Brothers case) Smith-Corona argued that Brothers is a foreign corporation (51% is owned by Japanese), but Brothers maintained that Smith-Corona is a foreign corporation because their products are made in Asia. Ownership does not really matter. For tax purposes, Honda of America Manufacturing (OH) is an American company. Only foreign firms pay tariffs and are subject to import quotas. Apple: 98% of iPhones are produced by Chinese contractors. 90% of Apple products are produced in China (Hence, Apple is a foreign company, subject to US tariff. Tim Cook is an American CEO, and hence Apple is often treated as an American company. Ownership criterion is irrelevant in most cases, except when calculating tariffs. DuPont was founded as a gunpowder manufacturer in 1802 by E. I. du Pont, who fled France during the French Revolution in 1789. du Pont family's net worth: $16B. Invented nylon and kevlar. DuPont De Nemours' net worth is $31B. |

| Nationality mix of headquarters managers | An international company is multinational if the managers of the parent company are nationals of several countries. Usually, managers of the headquarters (e.g., GM, Toyota) are nationals of the home country. This may be a transitional phenomenon. Japan's New Business Language (Rakuten, Japan's largest online firm with 100 million users, Amazon.com has 330 million users.) On March 1, 2010, Hiroshi Mikitani, chief executive, everything at Rakuten, from meetings to menus, would be in English. (Financial Times, December 17, 2017). All staff were given two years to improve their English proficiency. Very few companies pass this test currently. |

Business Strategy |

Sabvei(Subway) in Moscow. Global profit maximization: some are home country oriented, others are host country oriented. Successful firms: world-oriented , but must adapt to local markets. |

Root's definition

|

According to Franklin Root (1994), an MNC is a parent company that (i) engages in foreign production through its affiliates located in several countries, (ii) exercises direct control over the policies of its affiliates, and (iii) implements transnational business strategies in production, marketing, finance and staffing in a way that transcend national boundaries. In other words, MNCs exhibit no loyalty to the country in which they are incorporated. |

| Example | Barilla has plants and offices in Greece, France, Germany, Norway, Russia, Sweden, Turkey, US, and Mexico. Wheat is purchased from around the world. |

| Reference | Howard V. Perlmutter, "The Tortuous Evolution of the Multinational Corporation," Columbia Journal of World Business, 1969, pp. 9-18. |

-

3. Motives for Foreign Direct Investment (FDI) Anecdotes on Sunzi, who wrote "The Art of War." (Know your rivals and yourself and you always win in a battle.) Sunzi (544-496 BC) was a native of Ch'i, but served under King of Wu during the Spring and Autumn period (771- 476 BC). New MNCs do not pop up randomly in foreign nations. They are the product of conscious planning by corporate managers. Investment flows from regions of low profits to those of high returns. 1 Growth motive A company may have reached a plateau satisfying domestic demand, which is not growing. Looking for new markets.

Continued investment in the Home country yields diminishing returns.

2 Bypass protection in importing countries Foreign direct investment is one way to expand. FDI is a means to bypassing protective instruments in the importing country.

Examples:

(i) European Union: imposed common external tariff against outsiders. Multinational companies circumvented these barriers by setting up subsidiaries . JBS USA is a subsidiary of a Brazilian company, the world's largest meat processor of beef and pork. (It kills 5000 heads of cattle per day.)

(ii) Japanese corporations built auto assembly plants in the US, to bypass VERs.

3. avoid high corporate tax US corporate tax = 35% (21% in 2018) if income exceeds $335,000, Greece = 29%, France = 34%, Germany = 32%. Corporate tax rates are much lower in most other countries.

Comparison of effective tax rates is not meaningful, because MNCs park some profits offshore to avoid taxes. US = 19%, Japan = 22%

Tax competition: TSMC and Intel are building chip factories (Intel Fab) in Arizona. Samsung asks Texas for tax holiday for 15 years.

4. avoid high transport costs Build factories where consumers are. China produces 24 million cars. USA produces 4 million cars.

Transportation costs are like tariffs in that they are barriers which raise consumer prices. When transportation costs are high, multinational firms want to build production plants close to either the input source or to the market in order to save transportation costs.

Giant Container Ship Blocking Suez Canal Finally Shifts

Multinational firms (e.g. Toyota) are better off establishing factories where consumers are located than shipping goods to faraway counries.

5 avoid Exchange Rate fluctuations Japanese firms (e.g., Komatsu) invest here to produce heavy construction machines to avoid excessive exchange rate fluctuations. Also, Japanese automobile firms have plants to produce automobile parts. For instance, Toyota imports engines and transmissions from Japanese plants, and produce the rest in the U.S.

Toyota is behind GM and Volkswagen in China, and plans to expand its production in China (in addition to Tianjin and Guangzhou) and has no plans to build more plants in North America. (China's autoparts are cheaper.) It may have been a mistake for Toyota to overexpand its plants in the US. GM and Volkswagen have expanded their production plants in Shanghai.

A Komatsu machine used in ethanol production in Ida Grove, Iowa.

6 reduce competition The most certain method of preventing actual or potential competition is to acquire foreign businesses. GM purchased Monarch (GM Canada) and Opel (GM Germany). It did not buy Toyota, Nissan, and Volkswagen. Subsequently, they became competitors. Toyota is #1 in the car industry at present. Market shares of car companies in 2018 are:

GM = 17%, Toyota, Ford (joint second) = 14%, Hyundai-Kia: 9%.

World = 90 million cars. China = 24 million, US =11 million.7 secure essential inputs A foreign country may have the necessary resources (e.g., rare earth elements ).

REEs are critical to US military technology. LED and OLED displays use REEs. Yttrium is used in atomic batteries (long life batteries are needed to power guided missiles).

Since 1995, China is the dominant owner of REEs, extracting 85% of the world REEs.

Chinese barge shipping rare earth minerals ©8. secure technology transfer China's plan to buy up foreign technology meets increasing resistance from US and Europe (Catherine Wong and Zhou Xin) 9. cheap labor United Fruit has established banana-producing facilities in Honduras. Due to high transportation costs, FPE does not hold. ⇒Cheap foreign labor. Labor costs tend to differ among nations. MNCs can hold down costs by locating part of all their productive facilities abroad. (Maquildoras)

Komatsu first established its European factory in Belgium in 1967, and its American subsidiary in 1970. Over the years it established many other subsidiaries throughout Europe, Russia, America and Asia.

| 2. Three Stages of Evolution | |

| Export Stage | (i) initial inquiries ⇒ result in first export. (ii) Initially, firms rely on export agents. ⇒ expansion of export sales (iii) ⇒ foreign sales branch or assembly operations are established (to save transportation costs) |

| Foreign production stage | Why? (i) There is a limit to foreign exports, due to tariffs, quotas and transportation costs. (ii) Wage rates may be lower in LDCs. (iii) Environmental regulations may be lax in LDCs (e.g., China). Itai-Itai (meaning: ouch ouch) disease in Japan since the 1920s was caused by chromium-6 poisoning. Contaminated effluents leaked into rice paddies and water source.) Watch the movie, Erin Brochovich. (Hexavalent Chromium) (iv) meet Consumer demands in the foreign countries (v) mining industry is often located at the source. |

FDI versus Licensing Once the firm chooses foreign production as a method of delivering goods to foreign markets, it must decide whether to establish a foreign production subsidiary or license the technology to a foreign firm. |

|

| Licensing |

Licensing is usually the first experience (because it is easy) e.g.: Kentucky Fried Chicken in the U.K. Licensing does not require any capital expenditure Financial risk is zero. royalty payment = a fixed % of sales

The licensee may transfer industrial secrets to other independent firms, thereby creating rivals or copycats. In order to deter entry of copycat producers, MacDonalds may supply American ingredients or raw materials (e.g., beef) |

| copycats, knockoffs |

MacDonald has not openened its chain in Iran. |

| Foreign Direct Investment (FDI) |

It requires the decision of top management because it is a critical step. (i) it is risky (lack of information, large capital requirement) Robbery rates: US firms tend to establish subsidiaries in Canada first. Singer Manufacturing Company established its foreign plants in Scotland and Australia in the 1850s. (ii) plants are established in several countries. (iii) licensing is switched from independent producers to its subsidiaries. (iv) export continues (exports and FDI may be substitues or complements). When yen is weak, exports become more important that foreign production.) |

| Multinational Stage | The company becomes a multinational enterprise when it begins to plan, organize and coordinate production, marketing, R&D, financing, and staffing. For each of these operations, the firm must find the best location. |

Global

500 (2008) Wall-Mart |

|

How to tell whether a firm is multinational? Rule of Thumb |

A company whose foreign sales are 25% or more of total sales. This ratio is high for small countries, but low for large countries, e.g. Nestle (98%: Dutch), Phillips (94%: Swiss). Examples: Manufacturing MNCs 21 of top fifty firms are located in the U.S. 12 are in China 3 in Japan (shrinking) Petroleum companies: 6/10 located in the U.S.

|

Problem:

the parent firm cannot exercise any managerial control over the licensee.

(it is independent.)

Problem:

the parent firm cannot exercise any managerial control over the licensee.

(it is independent.)

-

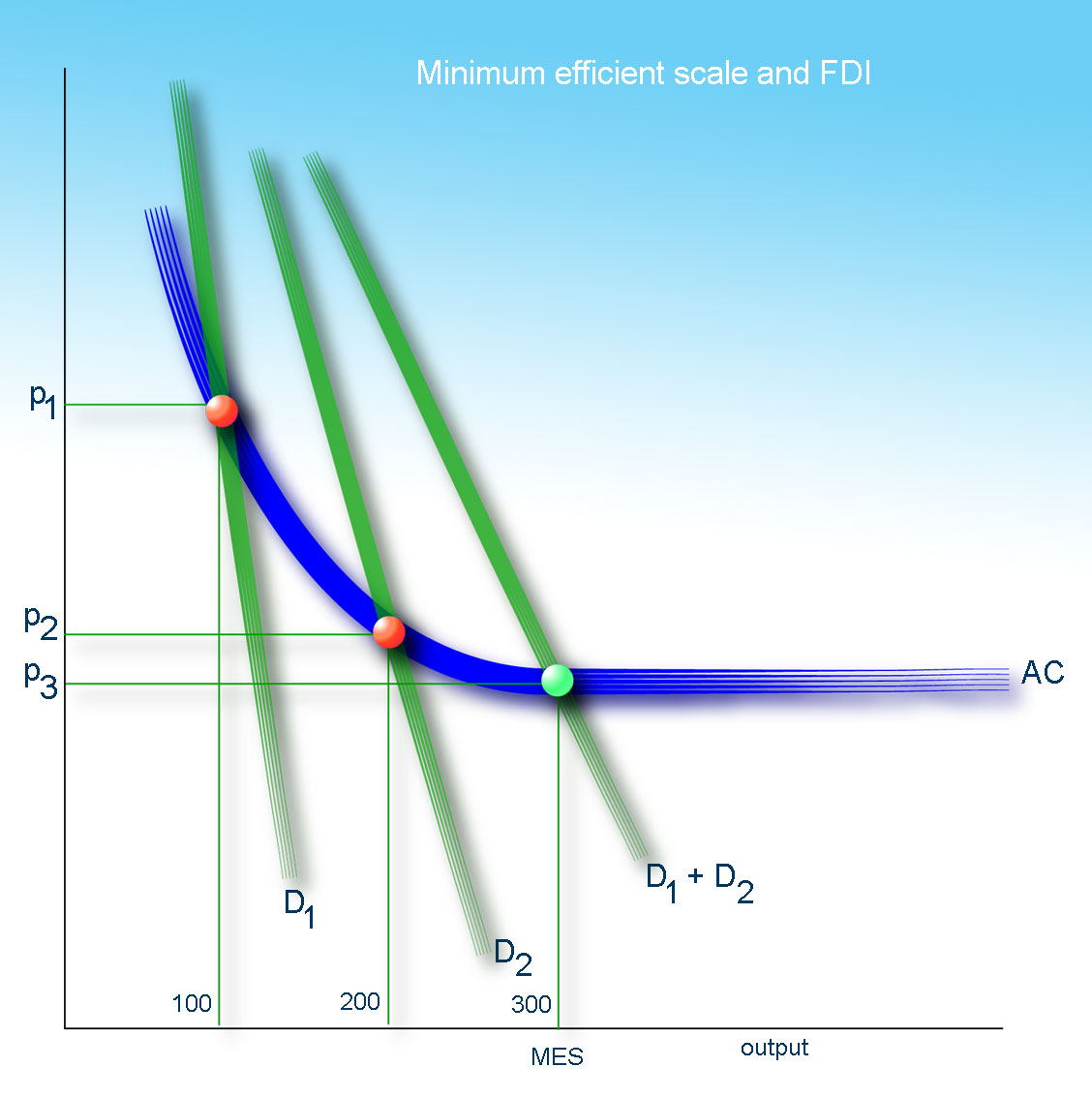

4. Export versus FDI Foreign production is not always an answer. Foreign markets can be better served by exporting, rather than by creating a foreign subsidiary if there are economies of scale. If large scale production reduces unit cost and transportation costs are not high, it is better to concentrate production in one place. MES MES is the minimum rate of output at which Average Cost (AC) is minimized. If minimum efficient scale (MES) is not achieved, then export.

In other words, if there exists excess capacity, why not utilize it and export outputs to other countries? There is no point in creating another plant overseas when domestic capacity is not fully utilized.

If foreign demand exceeds the minimum efficient scale, then FDI.

If demand is less than MES, do not build a foreign production plant.

- Anglo-Iranian Oil Company => was nationalized in 1951:

- National Iranian Oil Company

- Suez Canal was built by Suez Canal Company (opened in 1869), which was to operate it for 99 years. Nasser nationalized it 1956, 12 years before the lease expired.

- National Iranian Oil Company

| 5. International Joint Ventures | |

| What is JV? | JV is a business organization established by two or more companies that combines their skills and assets. |

Three forms

|

(i) A JV is formed by two businesses that conduct business in a third country. (US firm + British firm jointly operate in the Middle East) (ii) joint venture with a local firm, e.g., GM + Shanghai Automotive Industry Corporation (SAIC) = Shanghai GM. (plan to build factories to produce 5 million cars a year. 3 million cars in 2018) China requires foreign auto companies to form joint ventures and transfer technology to local Chinese partners. (iii) joint venture partner includes a local government. |

| Why form JV? | (i) Large capital costs - costs are too high for a single company (ii) Protection - LDC governments close their borders to foreign companies. JV bypasses protectionism. (iii) cut through red tapes (with state owned enterprises). e.g.: US workers assemble Japanese parts. The finished goods are sold to the US consumers. |

| Problems | (i) Control is divided. The venture serves "two masters" (ii) Forced Technogy Transfer (VP Mike Pence's speech): JVs in China requires transfer of technologies that were developed with long term US investments. China weighs law to curb forced technology transfer (People's daily). (iii) MNCs must comply with demands of the foreign government. e.g., Google in China Decoupling from China: US' attempt to move out of China. |

| Temptation of Nationalization | Effect of Nationalization (confiscation): Hugo Chávez of Venezuela nationalized: (a) the cement industry in 2008, Venezuela's crisis: corruption, shortages, despite its oil reserve of about 300 billion barrels. Hyperinflation: 13,000 percent. slash five zeros. Egypt nationalzes the Suez Canal (1956) |

| Welfare effects | (i) The new venture increases production, lowers price to consumers. (ii) The new business is able to enter the market that neither parent could have entered singly. (iii) Cost reductions (otherwise, no joint ventures will be formed) (iv) increased market power => not necessarily good for consumers. |